Applying for a personal loan can feel overwhelming, especially when you’re not sure what lenders are actually looking for. However, once you understand the main factors that affect your eligibility, the process becomes much simpler. In this guide, we’ll break down the credit score, income level, debt ratio, and other important things that can determine whether you qualify for a personal loan or not.

📌 First Things First: Why Qualification Matters

Before you even start filling out applications, it’s important to know what makes someone eligible. This can save you time and protect your credit score from unnecessary hard inquiries. Plus, by knowing where you stand, you can increase your chances of getting approved with a lower interest rate.

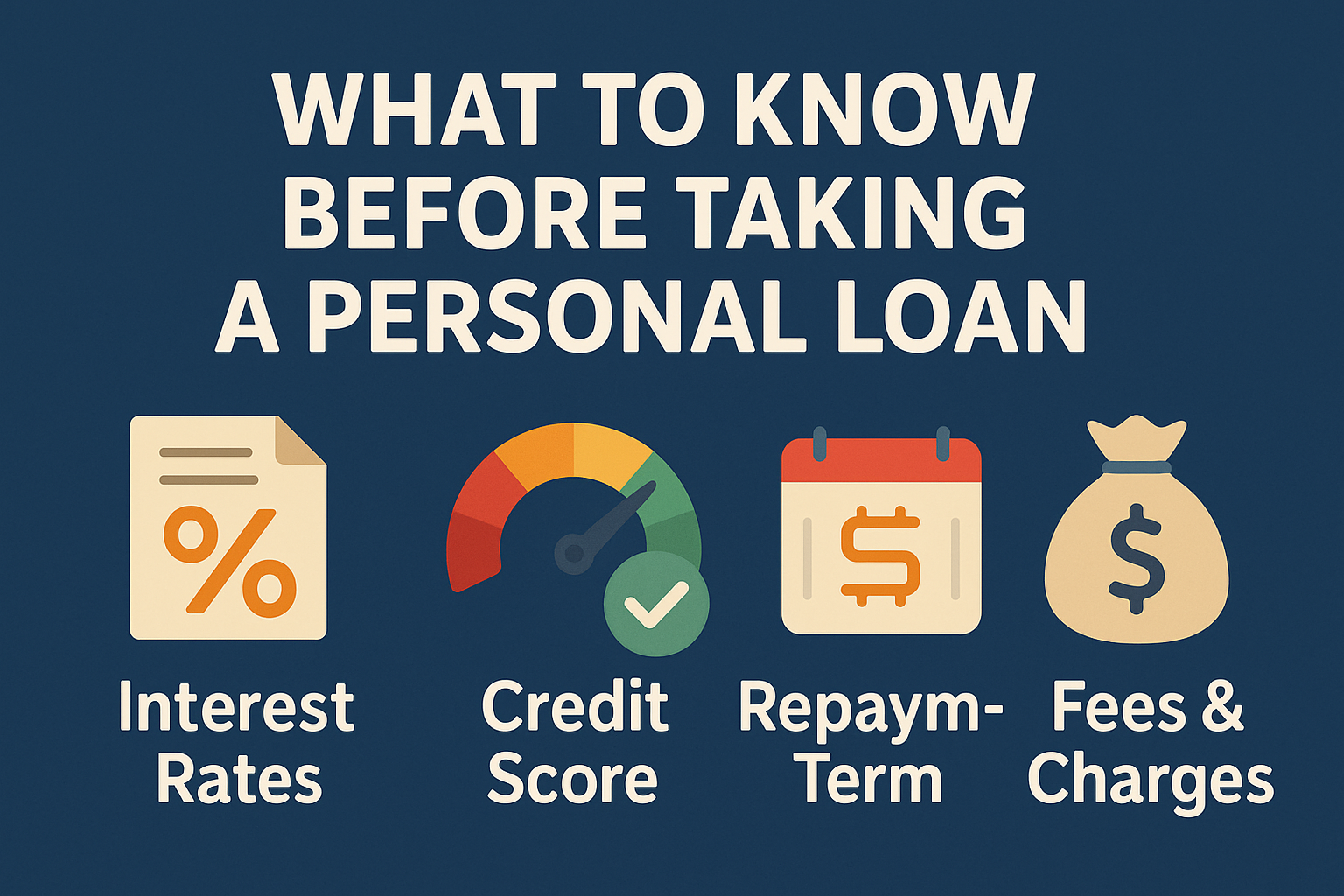

💳 1. Credit Score – The Most Important Factor

To begin with, your credit score is usually the first thing lenders check. It gives them an idea of how responsible you are with money. Typically, a score of 670 or higher is considered good, although some lenders may approve you with a lower score—especially if other factors are strong.

Furthermore, credit history also matters. Lenders prefer borrowers who have a track record of timely repayments, low credit utilization, and diverse credit types.

👉 Tip: Check your credit score for free on AnnualCreditReport.com or through apps like Credit Karma.

💵 2. Income – Can You Afford to Repay the Loan?

In addition to your credit score, lenders will look at your income. After all, they need to know that you can make your monthly payments on time. Whether you’re employed, self-employed, or have a consistent side income, what matters most is stable and verifiable earnings.

Generally, higher income improves your approval odds. That said, if you have low income but minimal debt, you may still qualify.

📉 3. Debt-to-Income Ratio (DTI) – Keep It Low

Another major factor is your debt-to-income ratio, or DTI. This is the percentage of your income that goes toward existing debt. Most lenders prefer a DTI under 36%, though some might go as high as 43%.

To calculate your DTI:

Total Monthly Debt Payments ÷ Gross Monthly Income × 100 = DTI

So, if you’re already juggling multiple loans or credit card payments, consider paying some of them off before applying.

🗂️ 4. Employment History – Stability Counts

In many cases, lenders will ask for proof of employment. Having a steady job—especially if you’ve been with the same employer for over a year—can improve your chances of qualifying. On the other hand, if you’ve changed jobs frequently, be ready to explain those changes.

🧾 5. Documentation – Be Prepared

Even if you meet all the criteria above, missing documents can delay or derail your application. That’s why it’s smart to prepare everything in advance, including:

- Government-issued ID

- Recent pay stubs or tax returns

- Bank statements

- Proof of address

- Social Security number

🧠 Final Thoughts: Get Ready Before You Apply

To sum it all up, qualifying for a personal loan is more than just clicking a few buttons online. It involves a combination of creditworthiness, income stability, and financial responsibility. Therefore, it’s best to review your credit report, pay down existing debt, and gather your documents before applying.

Once you’re ready, compare offers from multiple lenders. You can check prequalification tools that let you preview interest rates without impacting your credit score.

🔗 Helpful Resources

External Links:

- AnnualCreditReport.com – For free credit reports

- NerdWallet’s Loan Calculator – Estimate your monthly payments

Internal Links:

Leave a Reply